Some KiwiSaver funds could be less liquid than they claim.

At $55 billion, KiwiSaver is about the size of a third of all shares listed on the NZX. That is big enough to hide a multitude of “assets”. Like the dark web, you need to dig deeper than the fund updates and use forensic expertise to decipher what funds hold, but if you look, this is what you will find.

Each KiwiSaver manager is required to calculate an asset liquidity ratio quarterly. The main test of whether an asset is liquid is whether it can be sold in 10 working days at close to its stated value. Illiquid assets are any investment that cannot be sold within that period and private assets, such as unlisted property or private equity.

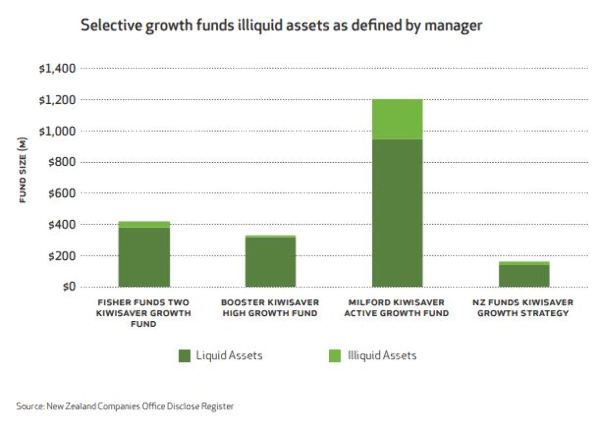

Based on our analysis, as at March 2019 Fisher Funds TWO KiwiSaver Growth Fund was an investor in unlisted property, holding 6.62% or $27.8 million. The problem with unlisted property is that there is no arm’s length daily price at which investors can transact. Investors entering and exiting funds which hold illiquid assets are therefore not treated equally. The conventional wisdom is that this is acceptable for the greater good.

However, at extreme points in the cycle illiquid assets can become difficult, if not impossible, to price, buy or sell.

The Fisher Funds schemes have also lent money to a private company, Tax Traders Limited. We estimate that as at the end of March they had lent more than $150 million. This debt appears to have been privately placed to one or two holders. It is difficult to determine whether they have classed this as an illiquid or liquid security. It is certainly an unusual investment.

Another holder of private assets is the Booster KiwiSaver Scheme. Booster has a number of unique aspects to their scheme. We have previously written about two of these – one of their other public funds lending $8.0 million to leverage shares in their KiwiSaver Geared Growth Fund, and their use of a creatively structured exit fee.

Booster lists 22 private assets in its High Growth KiwiSaver Fund. Most appear to be wine related. At least one of these assets were purchased out of receivership with funding provided in part by their KiwiSaver scheme.

A number of these 22 private assets appear to be related entities, such as Sileni Winery Building, Sileni- Plant and Equipment and Seleni Wines Limited Partnership. This raises some interesting questions. Are these really separate investments? Can one be sold without the other or without impacting the others’ price? These are questions an adviser might like to mull over. Of equal interest is that, despite the 22 private assets summing to over 5% by our math, Booster discloses an asset liquidity ratio of 96.92% for this fund at March end.

We estimate that the Milford KiwiSaver Active Growth Fund has 2.15% of private equity holdings. This fund has the look and structure of a well-diversified portfolio of private equity holdings. If KiwiSaver schemes are going to invest into private equity, then in our view Milford’s approach is a good example of how it should be done.

Those who live in glass houses should not throw stones, so the report is not complete without disclosing NZ Funds’ own illiquid holdings which in the case of the NZ Funds KiwiSaver Growth Strategy, sum to 13.53%. Our holdings are in hedge funds which have notice periods to exit, and are therefore treated as illiquid.

However, the big difference between our investments and private assets is that our investments can be readily priced. When we invest in hedge funds, we ensure that the underlying investments are market listed securities which can be priced daily.

On a more general note, it appears as though many managers assume that if a company is listed it is liquid, only some seem to be taking daily liquidity into account. The average daily volume that some shares can be sold at without moving the share price indicates otherwise. The FMA have signalled that illiquid assets will be one of their focus areas. Their oversight will be timely.

A copy of the latest Product Disclosure Statement for the scheme is available on request and at www.nzfunds.co.nz.

Michaels’ comments are of a general nature, and he is not responsible for any loss that any reader may suffer from following it.